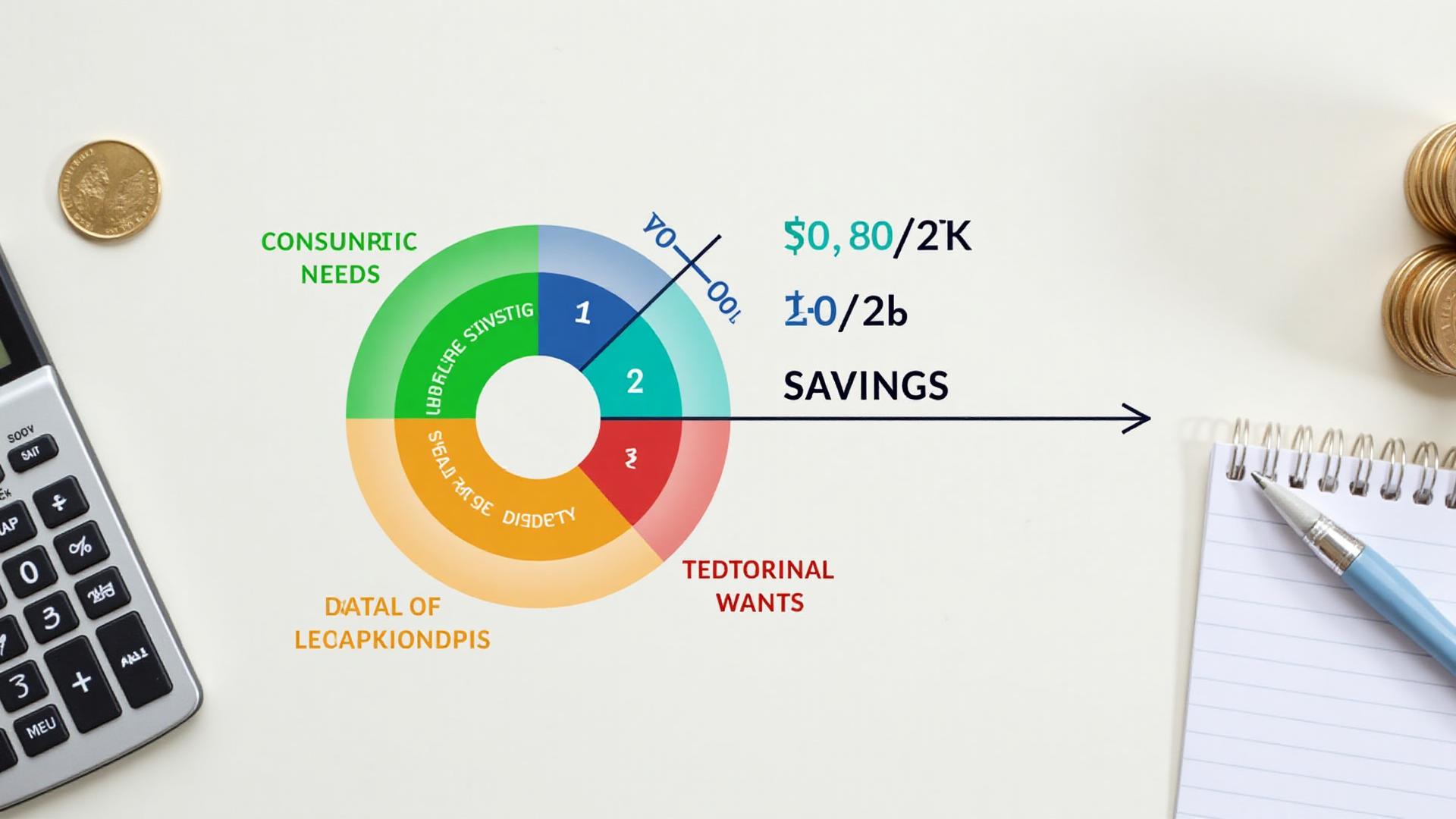

What Is the 50/30/20 Rule?

The 50/30/20 budget rule, popularised by Senator Elizabeth Warren, suggests splitting your after-tax income into three categories:

50%

Needs

Essential expenses you can't avoid

30%

Wants

Lifestyle and discretionary spending

20%

Savings

Future you, debt payoff, investments

Why It Works (In Theory)

The rule provides structure without micromanagement. It acknowledges that life should be enjoyed (30% wants) while ensuring financial security (20% savings) without overspending on essentials (50% needs).

Why It Doesn't Always Work (In Reality)

If you live in London, earn below median income, or have dependents, 50% for needs might be laughable. Housing alone could consume 40–50% of your income. Here's how to adapt:

Adjusted Formulas for Real Life

60 / 20 / 20

High Cost of Living

- 60% Needs (rent + bills eat more)

- 20% Wants (tighten lifestyle temporarily)

- 20% Savings (prioritise future you)

50 / 20 / 30

Debt Payoff Mode

- 50% Needs

- 20% Wants (maintain sanity)

- 30% Savings + Aggressive Debt Payoff

70 / 20 / 10

Low-Income Survival

- 70% Needs (essentials dominate)

- 20% Wants (don't eliminate joy completely)

- 10% Savings (something is better than nothing)

Needs vs Wants: The Grey Zone

The hardest part? Deciding what's actually a "need." Here's a reality-check framework:

✓ Clear Needs

- → Rent/mortgage (can't negotiate short-term)

- → Utilities (heat, water, basic electric)

- → Groceries (not takeaways)

- → Transport to work

- → Minimum debt payments

- → Essential insurance (health, car if required)

✗ Wants Disguised as Needs

- ✗ £150/month phone contract (need a phone, not an iPhone)

- ✗ Premium gym (need exercise, not a spa)

- ✗ Dining out 'for convenience' (it's a want)

- ✗ New clothes 'I need something to wear' (most of us have enough)

- ✗ Subscription boxes (definitely wants)

Building Your Personal Budget Formula

- Calculate after-tax income — Use your actual take-home pay

- List true needs from your 30-day tracking — Be honest

- Calculate needs percentage — Total needs ÷ income

- Adjust the rule — If needs are 65%, your formula is 65/20/15

- Set category limits — This becomes your spending ceiling

Example: Real UK Budget

Sarah, 28, Manchester — £2,200/month take-home

Needs — 58% — £1,280

Wants — 22% — £480

Savings — 20% — £440

Sarah's formula: 58/22/20 — not the textbook version, but it works for her life.

Making It Stick

- Review monthly — Adjust as income or needs change

- Use sub-categories — Break "wants" into smaller buckets

- Build in flexibility — One bad month doesn't break the system

- Celebrate wins — Hit your savings target? Acknowledge it

"The right budget is the one you'll actually follow."

Adapt it. Own it. Stick to it.

Put It Into Practice

Ready to create your personalised budget formula? Use our Budget Calculator to input your income and expenses, and see how your numbers compare to the 50/30/20 rule.

Try Budget Calculator